The end of every month is, for a data hound like me, my favorite part of the month. Case Shiller home sale report, the National Association of Home Builders data around home-starts and permits pulled and the National Association of Realtors data on pending sales comes out. These are the numbers that indicate where the housing market is and possibly where it’s going. Important rental data can be found on sites like Zumper.com, a blog that posts what’s happening in rental markets nationwide. The picture the combined data demonstrates is one of high cost to buy and high cost to rent. Rising rents in particular are very concerning because high rents disproportionately affect lower income families.

Much has been made of rising interest rates and the slowdown of the housing market. While it is true that the purchase market is slowing under the weight of the largest rate increases in history, soaring prices and the ever-increasing lack of affordability, housing prices are still holding up. Sure, there are more price reductions and there was a decline month over month, but this can be attributed to the seasonality of late summer, back to school etc. and the fact that homes with negatives, ie: condition or location, are having to reduce to find a buyer. This is how it’s supposed to be. These are signs of normal market behavior [Find us on social media here]. The reason prices aren’t dropping equally across the board is because there are still too many buyers for the inventory available. If you question this, just take a trip to the mall and make note of how many babies, strollers, and pregnant women you see. Millennials are starting families en masse and they are looking for homes to raise them in. But inventory is not going up. On the contrary, it’s peaked and is declining. Regarding our local market of the Conejo Valley, inventory is down 10% since late July. It’s pretty hard to have prices decline substantially when there are still more buyers than homes.

Back to rents; according to Zumper, rent on a 2 bedroom apartment in New York City, the most expensive market in the country, jumped year over year by an unconscionable 46.7%! But they aren’t alone. Nashville is up 26.7%; Boise 11%; Glendale, AZ 24.1%; Greensboro, NC 31.8%; Tulsa 23.3% – I could go on… it’s mind bending. I just listed a 500 SF 2 bed/1 bath flat in the heart of the San Fernando Valley for $2,050/mo and have had no fewer than 60 inquiries. This is not good.

Back to rents; according to Zumper, rent on a 2 bedroom apartment in New York City, the most expensive market in the country, jumped year over year by an unconscionable 46.7%! But they aren’t alone. Nashville is up 26.7%; Boise 11%; Glendale, AZ 24.1%; Greensboro, NC 31.8%; Tulsa 23.3% – I could go on… it’s mind bending. I just listed a 500 SF 2 bed/1 bath flat in the heart of the San Fernando Valley for $2,050/mo and have had no fewer than 60 inquiries. This is not good.

The problem with high rent is that it keeps people from getting ahead, increases poverty, decreases disposable income and reduces the ability to save and stay out of debt. In Los Angeles, rent takes on average more than 50% of people’s weekly paycheck. We are becoming a nation of renters. Where once the road to the middle class and self-sufficiency meant a driveway and a 3 bed/2 bath home. Today, the road to the middle class is quickly become a fairy tale. For without home ownership as a vehicle to build personal wealth, most Americans won’t have a chance. Home ownership is and always has been, the clearest path to the middle class.

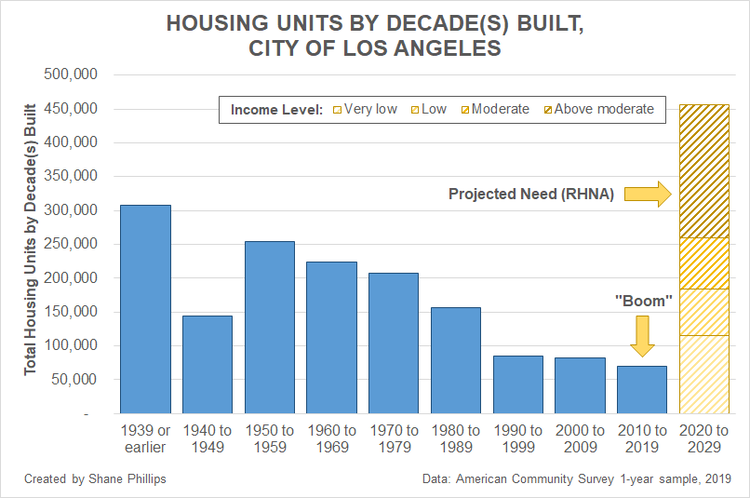

How did we get here? You don’t have to look any farther back than the Great Recession to find the bulk of your answers. We essentially stopped building new housing from 2008-2013. As a result, we are way behind where we should be to house our people. And if that weren’t troubling enough, consider what happened in 2012: Wall Street went into the single-family home landlord game. When the market began showing signs that it had bounced off the bottom, lenders like Bank of America, inexplicably unloaded all their bad debt and foreclosed homes to hedge funds and REITS. What’s even more galling is hedge funds like Blackstone and Invitation Homes as recently as 2017 received $1B in financing help to purchase an additional 48,000 single family homes, from none other than Fannie Mae, the government owned entity created specifically to help individuals achieve home ownership [See what your home is worth here]. Private equity firms like Blackstone, KKR, Apollo, Carlyle and REITS like Invitation Homes and American

For sale in Thousand Oaks!

Homes for Rent right here in Agoura Hills, now own more than 300,000 single family homes. And while that is only .02% of the roughly 94 million single family homes, they also own a quarter million manufactured homes and over 1 million apartments. But the numbers are even more disturbing because their ownership is not evenly spread out and instead concentrated in certain urban/suburban marketplaces. According to Americans for Financial Reform, private equity firms own 1 in 9 single family homes in Charlotte, 1 in 10 in Tampa, 1 in 12 in Atlanta. They also disproportionately target black owned neighborhoods where in 2021, 1 in 3 homes purchased in predominantly black zip codes went to institutional investors.  So defensive was Blackstone that in March of 2022, they posted a “Myth and Fact” page on their website disputing that they have a disproportionate influence and control over residential rents. With this kind of ownership concentration, is it any wonder buyers can’t find a home to buy? Private equity has been on a buying spree and are even partnering with home builders and buying entire subdivisions for rentals. That’s a whole ton of inventory that’s not for sale and a whole lot of rental property under the control of a very few. Think they might be able to raise rents at a whim without difficulty? You bet. Just look at the graph above at how much they’ve raised rents since Q4 2020. What’s even more crazy, is that all those private equity owned homes are occupied! They aren’t just vacant.

So defensive was Blackstone that in March of 2022, they posted a “Myth and Fact” page on their website disputing that they have a disproportionate influence and control over residential rents. With this kind of ownership concentration, is it any wonder buyers can’t find a home to buy? Private equity has been on a buying spree and are even partnering with home builders and buying entire subdivisions for rentals. That’s a whole ton of inventory that’s not for sale and a whole lot of rental property under the control of a very few. Think they might be able to raise rents at a whim without difficulty? You bet. Just look at the graph above at how much they’ve raised rents since Q4 2020. What’s even more crazy, is that all those private equity owned homes are occupied! They aren’t just vacant.

What’s it all mean? To my thinking it means we need to build more homes and do so fast. Call it national security. Call it national responsibility. Call it what you will, but understand, without the ability to buy and hold real estate, the wealth gap in America is going to grow exponentially and rents are only going to continue to skyrocket. It’s been said, that the role of government in a capitalistic society, is to control capitalism. Capitalism by definition is win/profit at all costs. Profit without regard for society. Don’t believe me? Check your history books [Contact Tim here]. It was because of this that in the early 20th century, the Federal Government began clamping down on monopolies.

What to do? Besides building, one solution to this issue would be to compel corporate home ownership to sell. One way to do this would be to impose a tax on corporate home ownership linked to the number of homes one corporation can own. Moreover, that tax would need to be progressive getting higher and higher as the number of units owned passes various thresholds. Without the progressive tax element, corporations will just pass the tax on to – you guessed it – renters. Think of it like a salary cap on professional sports teams: you can go over the cap but it’s going to cost you, big time. None of this is in lock step with the American dream of home ownership and the national wealth that is created through that home ownership. Neither is it consistent with the idea that success should be rewarded when someone like me proposes sweeping disincentive and crushing tax policy. But something must be done. We cannot dream of a land where the streets are paved in gold when, in fact, they are paved with rent checks.

In 1897 while traveling London, an article came out that Mark Twain had died. When asked by a reporter about this and his health, Twain replied, “Reports of my death have been greatly exaggerated.” So why this quote for a blog on and about real estate? Ahh.., because reports of the death of a seller’s market have been greatly exaggerated. Make no mistake, we are still in a seller’s market. Allow me to explain.

In 1897 while traveling London, an article came out that Mark Twain had died. When asked by a reporter about this and his health, Twain replied, “Reports of my death have been greatly exaggerated.” So why this quote for a blog on and about real estate? Ahh.., because reports of the death of a seller’s market have been greatly exaggerated. Make no mistake, we are still in a seller’s market. Allow me to explain.

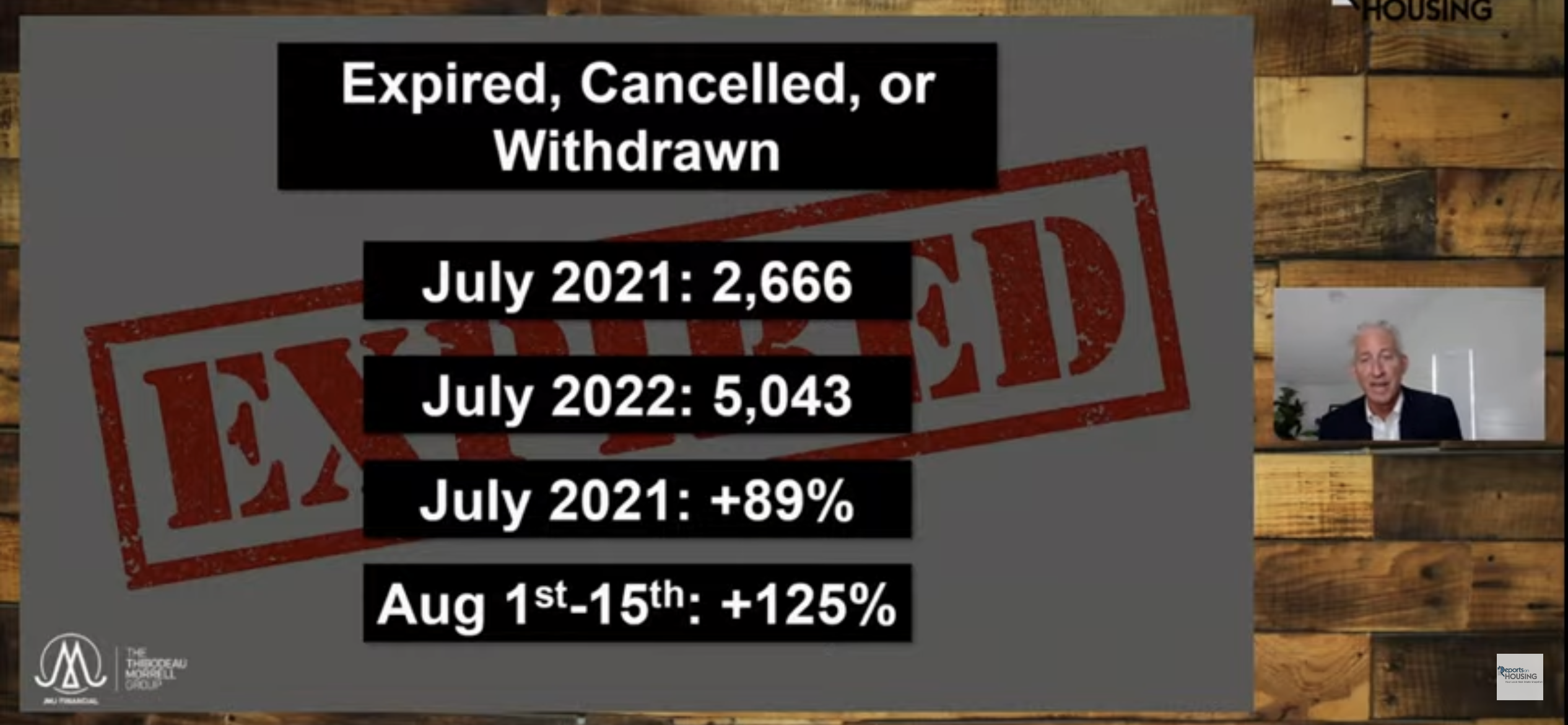

He goes on to say that amongst the many reasons that this has happened is that expired or cancelled listings are up 89% year over year!

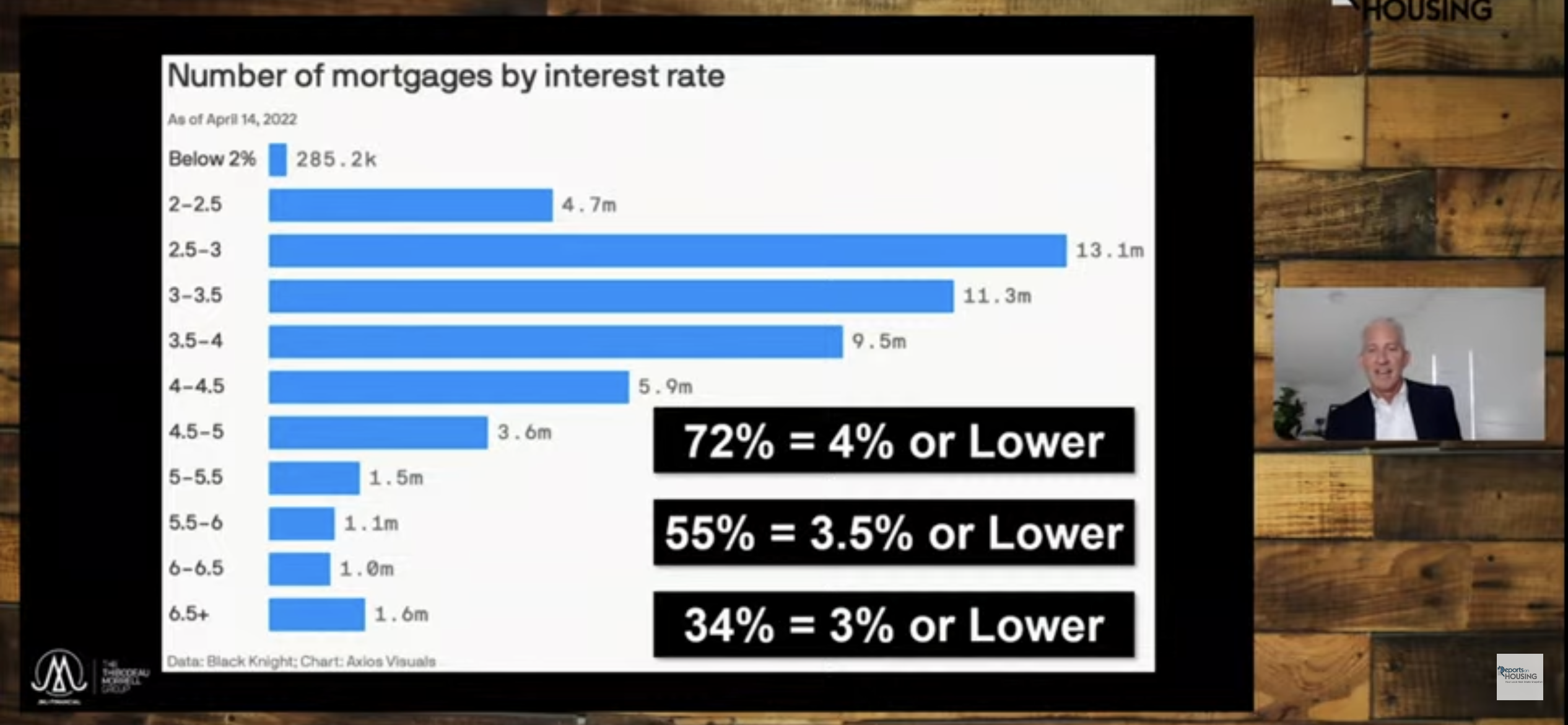

He goes on to say that amongst the many reasons that this has happened is that expired or cancelled listings are up 89% year over year!  He says that with 72% of all active mortgages below 4%, that sellers are simply electing to stay put rather than fight the current of an adjusting market.

He says that with 72% of all active mortgages below 4%, that sellers are simply electing to stay put rather than fight the current of an adjusting market.  Locally we see that the pending sales are down 15% and the number of homes for sale is up 15%. It’s the same 15%. This tight supply even in the absence of record high demand, is still woefully insufficient to cause the value of real estate to epically decline. Yes, we are seeing price cuts but this market behavior is consistent with a normal market. Historically prices rise in the spring and give some back in the fall. This is normal seasonal behavior. So, sellers who can no longer get what their neighbor got in the spring market, are having to reduce their price. There’s nothing unusual about that. Moreover, during the early part of 2022 inventory was at all time lows. In our local Conejo Valley, that number actually went below 100 homes for sale. In that environment, anyone with 4 walls and a kitchen could sell regardless of condition or location. This is no longer the case. Homes with warts or in locations that aren’t desirable or are in disrepair, are no longer selling at the sky-high prices. So here is a point of difference that’s not seasonal and strictly a situation being driven by the shift in interest rates, buyers’ affordability, and the fact that a slower market means more inventory [

Locally we see that the pending sales are down 15% and the number of homes for sale is up 15%. It’s the same 15%. This tight supply even in the absence of record high demand, is still woefully insufficient to cause the value of real estate to epically decline. Yes, we are seeing price cuts but this market behavior is consistent with a normal market. Historically prices rise in the spring and give some back in the fall. This is normal seasonal behavior. So, sellers who can no longer get what their neighbor got in the spring market, are having to reduce their price. There’s nothing unusual about that. Moreover, during the early part of 2022 inventory was at all time lows. In our local Conejo Valley, that number actually went below 100 homes for sale. In that environment, anyone with 4 walls and a kitchen could sell regardless of condition or location. This is no longer the case. Homes with warts or in locations that aren’t desirable or are in disrepair, are no longer selling at the sky-high prices. So here is a point of difference that’s not seasonal and strictly a situation being driven by the shift in interest rates, buyers’ affordability, and the fact that a slower market means more inventory [

provided you “Buy it right.” By this I mean, an appropriate discount from market price because when you go to sell, you have to discount it in the same way. What made our recent market unique was that the shortage of properties compelled some buyers to pay market for a challenged property and not buy with the appropriate discount. In a market like the one we were just in, everything sells. But in a normal market, that’s not how it works. And in a down market, that’s definitely not what happens. In a down market, there’s always a nicer home or better location that must sell at the same time and the discount you have to make often times ends up disproportionate. A home is only worth what a buyer will pay and if they can buy a better property than yours for “X” then you have to offer a discount to incentivize the buyer to buy yours.

provided you “Buy it right.” By this I mean, an appropriate discount from market price because when you go to sell, you have to discount it in the same way. What made our recent market unique was that the shortage of properties compelled some buyers to pay market for a challenged property and not buy with the appropriate discount. In a market like the one we were just in, everything sells. But in a normal market, that’s not how it works. And in a down market, that’s definitely not what happens. In a down market, there’s always a nicer home or better location that must sell at the same time and the discount you have to make often times ends up disproportionate. A home is only worth what a buyer will pay and if they can buy a better property than yours for “X” then you have to offer a discount to incentivize the buyer to buy yours.

the rarest of rare. This would be a view lot (rarest of all amenities), a large lot and a cul-de-sac lot [

the rarest of rare. This would be a view lot (rarest of all amenities), a large lot and a cul-de-sac lot [

into a recession in 2023.” What is this @Anchorman? They sound like Paul Rudd’s character Brian Fantana when he says of his panther cologne, “60% of the time, it works every time?” Seriously? If the economy is really in trouble prove it! And if there’s trouble on the horizon, how is it that continuing claims for unemployment (insurance) are at a level not seen since 1970 and still declining? That’s right, not going up, not leveling but still declining. We would realistically need to have 3 months with an average increase in unemployment of 3% or more, to indicate a recession is coming. There is no evidence of that.

into a recession in 2023.” What is this @Anchorman? They sound like Paul Rudd’s character Brian Fantana when he says of his panther cologne, “60% of the time, it works every time?” Seriously? If the economy is really in trouble prove it! And if there’s trouble on the horizon, how is it that continuing claims for unemployment (insurance) are at a level not seen since 1970 and still declining? That’s right, not going up, not leveling but still declining. We would realistically need to have 3 months with an average increase in unemployment of 3% or more, to indicate a recession is coming. There is no evidence of that. even if prices drop. “Why, you ask?” Why would you? Even if you’re financially under stress, you can always get a renter if you had to. And of course, if past experience portends to the future success, prices will eventually go back up (

even if prices drop. “Why, you ask?” Why would you? Even if you’re financially under stress, you can always get a renter if you had to. And of course, if past experience portends to the future success, prices will eventually go back up ( guidance when it comes to matters involving real estate. Rising rates are not the end of the world. Rising rates are the result of rising inflation and inflation raises all asset classes including real estate. This notion that rising rates is the death knell of real estate is simply as my mother would say, hogwash. But there’s no doubt that rising rates do and should alter they way we view a real estate purchase.

guidance when it comes to matters involving real estate. Rising rates are not the end of the world. Rising rates are the result of rising inflation and inflation raises all asset classes including real estate. This notion that rising rates is the death knell of real estate is simply as my mother would say, hogwash. But there’s no doubt that rising rates do and should alter they way we view a real estate purchase.

suspense. Alas, there is no suspense when it comes to housing. No, there’s no mystery here at all; we simply don’t have enough housing. And notice that I am carefully using the word housing, not homes. This is to emphasize that we have a structural problem, not just a problem of wealth inequality or a battle of the haves and have nots. We have not built enough shelter for our people and California is the worst, ranking at 49th in unit per resident ratio.

suspense. Alas, there is no suspense when it comes to housing. No, there’s no mystery here at all; we simply don’t have enough housing. And notice that I am carefully using the word housing, not homes. This is to emphasize that we have a structural problem, not just a problem of wealth inequality or a battle of the haves and have nots. We have not built enough shelter for our people and California is the worst, ranking at 49th in unit per resident ratio. comes to mind) and Small (Mom and Pops). Investors represented 17% of all buyers last month, squeezing out the would-be Millennials [

comes to mind) and Small (Mom and Pops). Investors represented 17% of all buyers last month, squeezing out the would-be Millennials [